Giving parents and students the freedom to choose.

PHILOSOPHY | STUDENT STORIES | MAP | FAQ | IMAGES | DONATE

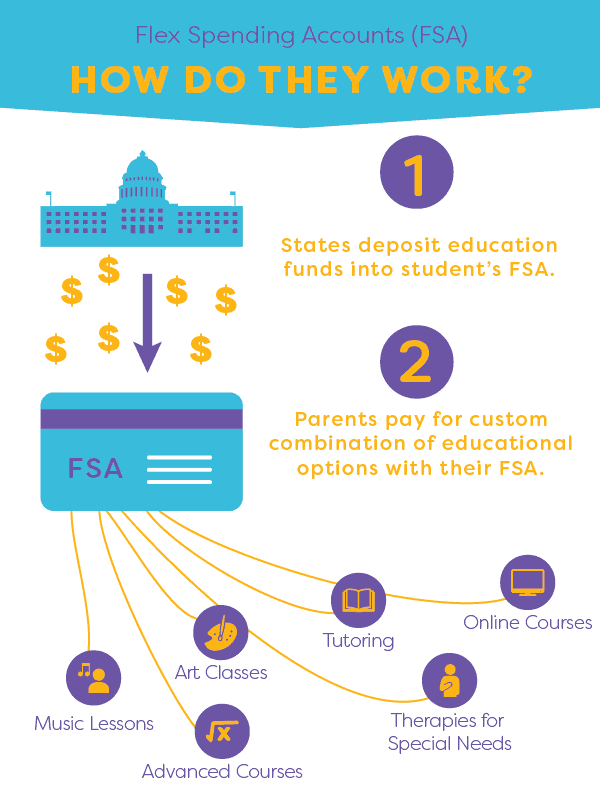

WHAT ARE FSAs?

Flexible Spending Accounts are private accounts managed by parents for use on educational expenses for their child. The state calculates a student’s per-pupil amount and makes deposits into the account. Parents can use account funds to pay for online classes, private school tuition, personal tutors, books and other curricular materials, or families can even save for college.

Scroll down to learn more about Flexible Spending Accounts and the benefits they could provide for students everywhere.

In defense of education choice

The world – and Utah – isn’t the same as it once was. Education shouldn’t be, either.

Over the last 10 years, our society has acquired a taste for customizing everything, as well as the innovations to do so. There is also a growing discomfort with our education system: a stagnant, highly regulated, one-size-fits-all, grade-by-age system that misses the mark for too many students and needlessly frustrates teachers out of the profession, creating teacher shortages.

THE STUDENTS

In 2011, Arizona passed a choice program much like the FSA plan we propose for Utah. Students who have special needs, those attending failing schools, children who have been adopted, students on tribal lands and others are already seeing the benefits of education choice. We want to tell you their stories.

AROUND THE COUNTRY

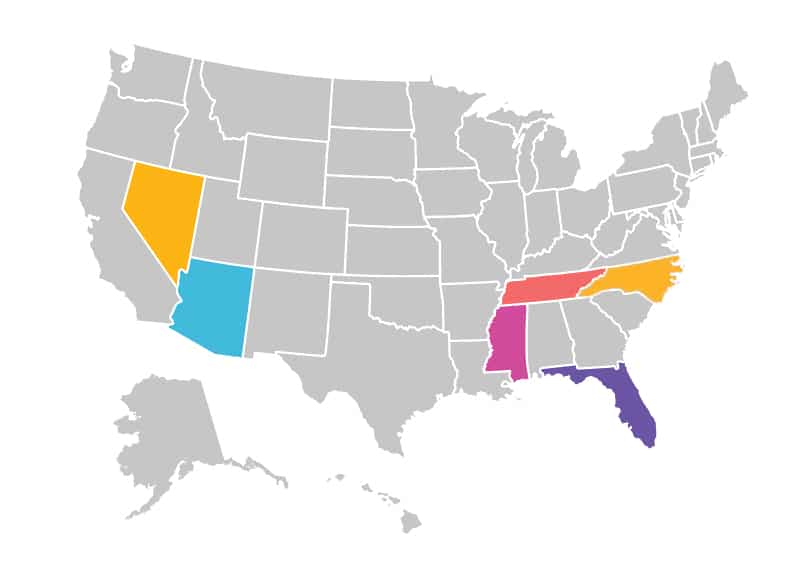

Today, six states from across the country have a law creating some form of Flexible Spending Accounts. Arizona was the first, establishing FSAs in 2011 under Arizona’s Empowerment Scholarship Account Program. Initially, Arizona’s program was only available to parents of children with special needs, but due to the FSAs’ popularity they were quickly expanded to children of active military parents; foster and adopted children; children in failing public schools; students residing on Native American reservations; and siblings of children with an account. In 2017, Arizona passed legislation that made all students eligible for the program.

Since 2011, Florida, Mississippi, Tennessee, Nevada, and North Carolina have passed legislation creating Flexible Spending Accounts. Click on our interactive map to learn more about FSAs in other states.

Q: What are flexible spending accounts?

A: Flexible Spending Accounts are private accounts managed by parents for use on educational expenses for their child. The state calculates a student’s per-pupil amount and makes deposits into the account. Parents can use account funds to pay for online classes, private school tuition, personal tutors, books and other curricular materials, or families can even save for college.

Q: What are the key provisions?

A: Flexible Spending Accounts are private accounts, and parents have direct control over the purchase of educational materials or services. Parents can choose from different learning experiences and materials. Unlike a school voucher, account funds are not mandated to flow directly from the state through a parent to a specific vendor. Funds can roll over to pay for college.

Q: What if a student doesn't go to college?

A: If a student doesn’t attend college, unused funds revert back to the state.

Q: Who decides what is an allowable expense?

A: The State Board of Education creates a “white list” of approved providers and services. Providers can ask to be included on the list. Parents can also ask for different services or providers to be on the list.

Q: What about fraud?

A: If parents misuse funds (spend them on unapproved providers or services) subsequent funds are suspended or used to pay for the misuse of funds. The state can audit the accounts.

Q: Does this take money from the public system?

A: Flexible Spending Accounts use currently allocated education funds and simply allow those funds to follow the child to a variety of education options. The public school system retains the funding needed for fixed overhead costs and/or administration of the program.

In public schools there are both fixed and variable expenditures. Very often opponents of education choice policies focus on the fixed costs when students leave, but focus on the variable costs when more students enroll. The truth is all costs are variable in the long run and schools already experience fluctuations in enrollment.

Q: How are children who remain in the public school affected?

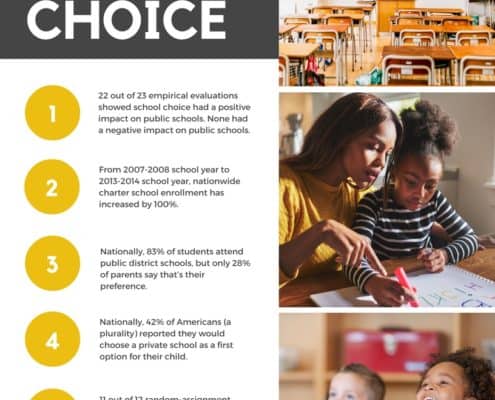

A: Flexible Spending Accounts allow for public schools to be more responsive to students who choose to remain in a given school. There is no evidence that any educational choice law has had a negative impact on public school students. In fact, 22 out of 23 studies from respected researchers at Harvard, Stanford, Northwestern University, the University of Arkansas, and more have found small but statistically significant positive impacts on the performance of public school students after the introduction of school choice laws. One study found no measureable difference. None found any harm.

Q: Where can I find further research?

Q: What is the difference between a Flexible Spending Account and a school voucher?

A: School vouchers allow parents to use public funds to pay private school tuition. A state agency issues a check, similar to a coupon, which is endorsed by a parent and turned over to a private school – or the check can be issued directly to a school under the name of the parent(s). With Flexible Spending Accounts, parents can use student funds for many different expenses.

Q: Are Flexible Spending Accounts constitutional?

A: Yes. Shortly after the first spending accounts (called education savings accounts or ESAs in Arizona) were awarded to applicants in Arizona, several groups including the Arizona School Boards Association and the Arizona Education Association (a teachers union) filed suit to stop the program. Goldwater Institute attorney Clint Bolick represented the Goldwater Institute alongside the Arizona Attorney General’s office and the Institute for Justice in defending the program.

Oral arguments in Niehaus v. Huppenthal were held at the Maricopa County Superior Court on November 28, 2011, and Superior Court Judge Maria Del Mar Verdin issued a ruling on January 25, 2012, that found the spending accounts constitutional. In her opinion, Judge Verdin wrote, “The exercise of parental choice among education options makes the program constitutional.”

On October 1, 2013, the Arizona Court of Appeals also ruled in favor of the accounts. Judge Jon W. Thompson wrote, “The ESA does not result in an appropriation of public money to encourage the preference of one religion over another, or religion per se over no religion. Any aid to religious schools would be a result of the genuine and independent private choices of the parents. The parents are given numerous ways in which they can educate their children suited to the needs of each child with no preference given to religious or nonreligious schools or programs. Parents are required only to educate their children in the areas of reading, grammar, mathematics, social studies, and science.”

On March 21, 2014, the Arizona Supreme Court upheld the appeals court ruling, declaring the program legal in the face of the Blaine Amendment, which exists in nearly 40 states, prohibiting the transfer of government money to a private or parochial school. While the Arizona decision does not guarantee courts in other states will rule in the same way, Niehaus v. Huppenthal provides valuable case law for lawsuits filed against similar policies.

Likewise, in 2016 the Nevada Supreme Court held that Nevada’s universal spending account was constitutional, notwithstanding challenges about funds going to religious schools or for sectarian purposes. However, the court held that it did not adopt an “independent basis” to fund the program outside of the constitutionally protected funding for public schools, and is therefore “without an appropriation to support its operation.”

Q: Do states have to repeal their Blaine Amendments in order to enact an Education Savings Account program?

A: No. Education Savings Accounts were specifically designed to avoid conflicts with Blaine Amendments. Blaine Amendments prohibit public money from being appropriated in aid of private or sectarian schools. Under the program, the only appropriation the state makes is into privately managed accounts. Not a dime of the state’s appropriation is earmarked for private or sectarian school tuition.

If parents ultimately decide to purchase private school tuition with the funds, the wide scope of parental choice and control sufficiently distances the state from the choice. This distance in turn undermines any finding that the state is appropriating money to private or sectarian schools.

.

Q: If parents spend funds at a religious school, does that mean the program violates the separation of church and state?

A: No. To maintain a proper separation between the state and religion, state constitutions forbid the states from appropriating money directly to religious schools. But no such appropriation could occur under the Flexible Spending Account program. The state may only deposit money into privately controlled accounts. After it does so, the state no longer directs any of the funds. If a parent later chooses to spend savings account funds at a religious school, the state is entirely independent from that decision. That separation means the program does not violate any separation between church and state.

Q: Does participating in the Flexible Spending Accounts prevent students from returning to public schools?

A: No. Parents participating in the program must agree to not enroll their child in a public school while receiving spending account funds. This policy prevents double dipping of state funds. However, if at any point the parent decides the program is not meeting their child’s needs, the parent may return the funds and re-enroll their student in public school.

Q: What about the impact on teachers?

A: Flexible Spending Accounts enable teachers to be more innovative and flexible with how they educate children and provide them the opportunity to expand their impact to students across the state. As an added benefit, teachers would have the opportunity to earn additional income by tutoring, teaching online courses, and facilitating extracurricular options.

SHAREABLE IMAGES

Read More

What you need to know about the upcoming state party conventions

The two major political parties are about to hold their state conventions. Here’s what you need to know.

Here’s why the First Amendment’s religion clauses are not in conflict

Some suggest there is a tension between protection for the free exercise of religion and the prohibition on the establishment of religion. But a better take is to see the two clauses as congruent.

Is California’s minimum wage hike a mistake?

Is raising the minimum wage a good tool to help low-income workers achieve upward mobility? That’s the key question at the heart of the debate over California’s new $20 an hour minimum wage law for fast food workers.